How To Finance Your College Education

Updated February 28, 2024

Graduating Debt Free

Student loan debt is at a record high and every year reports and media headlines show that the problem is only getting worse. Loans may be a fast and convenient way to get money for a college education, but taking out too many loans and/or not having a solid payment plan in place can result in negative financial consequences that are felt long after the cap and gown have been hung. Debt—or at least overwhelming debt—doesn't have to be part of the higher education equation, however. This guide explores the various ways students and their families can finance a college education, from well-known avenues such as scholarships and grants to newer strategies that have emerged in the last decade to sources that many students simply forget to tap into. Also included is an interview with a financial aid expert and tips on how to effectively lower the overall cost of a college degree. With the right knowledge and proper planning, it is possible to graduate with manageable debt and, in some cases, eliminate it completely.

Meet the Expert

Sean Martin

Sean Martin is Director of Financial Services at Connecticut College in New London, Connecticut. Prior to his current position, Sean worked for 10 years as Athletic Director at Fairfield University and Boston College, and in the Financial Aid department at Wesleyan College, where he most recently served as Senior Associate Director.

Loan Alternatives: Ways to Pay for College

Student loan debt can have lasting consequences, but it's one that can be partially or entirely avoided. The trick is to identify alternate funding sources and there are several out there available to both undergraduate and graduate students. Below is a list of potential funding sources.

Crowdfunding

Crowdfunding is a way to raise money—and awareness—for a specific project or venture, usually through an online platform. It's a concept that is popular among the start up world, and many young people have recently adapted this method to raise money for a college education. The concept has actually been around in one form or another for decades, but it took the Internet to make it more practical and widespread.

Crowdfunding websites began showing up in the early-2000s and exploded a few years later with sites like Kickstarter and Indiegogo. Since then, crowdfunding to pay for college has taken off in a big way. Education crowdfunding sites are now plentiful and provide platforms for students to employ a variety of methods for raising cash for college or paying off student debt. Here's a look at some of the most popular and how they work:

GoFundMe

What is it: GoFundMe is a donation-based funding site dedicated to charity and personal money raising. Students or others can launch campaigns to pay for college-related costs including tuition, books, fees, living expenses, and to pay off existing student loans. Because GoFundMe is donation-based, funds raised here need not be repaid.

Cost: 5 percent service fee and 2.9 percent (plus $0.30 per donation) processing fee.

Indiegogo

What is it: The Indiegogo platform is open to anyone that wants to raise funds to finance a project, including paying for education. Funding decisions are borrower- and lender-driven and Indiegogo does not decide which projects are worthy and which are not. Individuals simply set an amount to be raised, explain the purpose of the funds, then activate their campaign. The platform works on a reward-based system, meaning that donors may receive a gift in exchange for their donations.

Cost: Indiegogo collects 9 percent of funds raised, returning 5 percent to campaigners if the campaign reaches its goal, for a total service fee of 4 percent. If a campaign fails to reach its goal, the campaigner keeps the funds raised, but Indiegogo holds onto the entire 9 percent charge. Alternatively, in fixed funding campaigns that fail to meet the goal, all funds raised are returned to donors and Indiegogo keeps nothing. Third-party (credit card or PayPal) processing fees of 3-5 percent apply.

Piglt

What is it: Piglt (pronounced "piglet") is a crowdfunding site specifically for education-related campaigns. Borrowers (called “Dreamers”) create video campaigns to explain their projects to lenders (“Believers”). Dreamers offer incentives in the form of unique skills, abilities, or products in exchange for funds. Dreamers may raise money for practically any education-related project, including payment for tuition or existing student loans, or to fund academic activities such as classes, seminars, or mentoring programs.

Cost: 3 percent payment processing fee plus 5 percent if the Dreamer reaches the funding goal, or 8 percent if a loan campaign fails to reach its goal and the Dreamer keeps the moneys raised. No fees for a tuition campaign that fails to meet its goal, but all moneys raised are refunded to Believers.

Upstart

What is it: The Upstart platform allows borrowers to obtain unsecured funding through fixed loan rates. It uses a unique set of factors such as school attended, area of study, academic performance, and employment history to determine loan amounts. Loans are paid back based on a percentage of the student's future income.

Cost: 1 to 6 percent of the target loan amount, charged as a one-time non-refundable fee that is deducted from the loan proceeds prior to their release to the borrower.

Military Benefits

Active military and veterans enjoy plenty of higher education benefits. Here's a look at the most popular options:

Tuition Assistance

The Army, Navy, Marines, Air Force, and Coast Guard each offer a tuition assistance program for its service members. Tuition assistance covers up to 100 percent of college tuition and fees to a maximum of $4,500 annually. Benefit and eligibility details vary by service branch.Post-9/11 GI Bill

The Post-9/11 GI Bill is available to service personnel, Reserve and Guard members, and veterans who served for at least 90 consecutive days on or after September 11, 2001 or were honorably discharged with a service-related disability after 30 days of continuous service after September 11, 2001. The maximum payable educational benefit depends on the service member's length of active duty service. Eligible individuals may receive up to 36 months of educational assistance, which can be used to cover the cost of not only postsecondary education expenses, but also on-the-job training, flight schools, tutorial assistance, certification tests, and licensing fees.Yellow Ribbon Program

The Post-9/11 Bill may also cover the entire cost of in-state tuition and fees at public postsecondary institutions that participate in the Yellow Ribbon Program. Unused educational benefits may also be transferred to a spouse or dependent, based upon the service member's agreement to serve an additional four years.Loan Repayment

The military may partially or fully repay a service member for his or her student loans. Loan repayment is handled differently by each service branch, but in most cases, programs are open to enlisted personnel only. Other eligibility factors include occupational specialty (MOS), terms of the service member's contract, and loan status (loans cannot be in default).Montgomery GI Bill

The Montgomery GI Bill (MGIB) offers up to 36 months of higher education benefits to eligible service members. For active duty members and veterans, monthly benefits paid are based on the type of training enrolled in, length of service, category, any college fund eligibility, and if the service member contributed to the $600 buy-up program. Benefits can total over $1,500 per month for full-time students. Eligibility requirements for reserves include a six-year obligation to serve in the Selective Reserve and completion of initial active duty training.

Beyond the Benefits: Military & Veteran Scholarships

Afghanistan and Iraq War Veterans Scholarship

Sponsoring organization: AFCEA NOVA

Amount: Varies

Application due date: November 15, 2015

Merit-based scholarships will be awarded to active duty service members and honorably discharged U.S. military veterans who are enrolled part or full time at an accredited four-year college. Candidates must be pursuing a degree in one of the STEM fields listed on the site. Not open to high school students.

AMVETS/University of Phoenix Scholarship

Sponsoring organization: AMVETS National Scholarship Program

Amount: Varies

Application due date:

September 8, 2015

This program offers 20 full-tuition scholarships to honorably discharged veterans or current service members, a spouse of a current military service member or honorably discharged veteran, or a child under 21 or 23 years old of a current military service member or honorably discharged veteran. Recipients can attend University of Phoenix on-campus or online.

Army Scholarship Foundation

Sponsoring organization: Army Scholarship Foundation

Amount: $500 – $2,000

Application due date: Varies

Every year, the Army Scholarship Foundation awards various one-year financial aid scholarships. Recipients can renew awards annually for up to four years at an accredited educational or technical institution.

CCME Veteran Scholarships

Sponsoring organization: Council of College and Military Educators

Amount: $1,000

Application due date: October 15, 2015

Every year, CCME provides scholarships to active duty service members and veterans, as well as spouses of service members. There are three types of awards currently available—the Joe King Scholarship, Loretta Cornett-Huff Scholarship, and Veteran Scholarship.

CSM Virgil R. Williams Scholarship

Sponsoring organization: Enlisted Association of the National Guard of the United States

Amount:$2,000

Application due date: July 7, 2015

Applicants must be in good academic standing, be enrolled in Grantham University, and must be an EANGUS member (or spouse of an EANGUS member).

George and Vicki Muellner Foundation Scholarship

Sponsoring organization:AFA/George and Vicki Muellner

Amount:$5,000

Application due date: Varies

Open to Arnold Air Society and Silver Wing students for their undergraduate education. Two $5,000 awards are granted every year.

GIA Scholarship Fund for U.S. Veterans

Sponsoring organization: Gemological Institute of America

Amount: $1,500

Application due date: April 30 and June 15

Scholarships are awarded during two periods each year for online courses, programs, or lab classes in gemology, jewelry, and design. This award is open to U.S. military veterans and applicants must provide proof of U.S. military service.

Military Award Program (MAP)

Sponsoring organization: Imagine America Foundation

Amount: Varies

Application due date: June 30

Every year, the Imagine America Foundation offers awards to applicants enrolled in over 300 career colleges nationwide. Applicants must be active duty, reservist, honorably discharged, or retired veteran of the U.S. military.

National Military Family Association

Sponsoring organization: Varies

Amount: Varies

Application due date: Varies

In partnership with various institutions and organizations, NMFA offers several scholarship opportunities for military spouses. Users must register to gain free access to listed scholarships.

The American Legion Legacy Scholarship

Sponsoring organization: The American Legion

Amount: Varies

Application due date: April 15

Through the Legacy Scholarship Fund, financial assistance is offered to children whose parents died on active duty on or after September 11, 2001. Amount varies and recipients can re-apply.

Grants and Scholarships

In order to qualify for financial aid (including loans and grants), students and their parents need to complete the Free Application for Federal Student Aid (FAFSA®). The FAFSA® determines “Expected Family Contribution”, which is the amount each family is expected to contribute toward a student's education. This form is used by nearly every university to determine student eligibility for aid and to create individualized financial aid packages. A division of the U.S. Department of Education, Federal Student Aid is the single largest source of financial aid in the country, providing over $150 billion in federal loans, grants, and work-study funds to more than 13 million students annually.

Eligibility for financial aid

Specific eligibility requirements for federal financial aid vary by program, but students can use the following checklist as a starting point.

- Have a high school diploma, finish an approved homeschool program, or complete a General Education Development (GED) program

- Be approved to enroll in an accredited degree or certificate program at a postsecondary institution

- Have a valid Social Security number

- Register with Selective Service (for male students between the ages of 18 and 25)

- Be a US Citizen or hold a Green Card, an Immigration Arrival Departure Record, T-Visa, or possess Battered Immigrant Status

- Maintain satisfactory academic progress in a postsecondary educational program

Scholarships and grants are one of the most traditional and familiar methods of financing a college education. Both are excellent sources of funding since there is no requirement to pay them back. Although the terms "scholarship" and "grant" are often used interchangeably, scholarships are generally thought of as merit-based awards, while grants are made based on the recipient's financial need.

Scholarships

Scholarships are non-government educational awards that can be used to pay for college-related expenses such as tuition, books, and fees, and do not need to be repaid. Students can find such opportunities through some of the following entities:

- Corporations

- Professional Associations

- Private organizations

- Foundations

- Nonprofits

- Industry associations and organizations

Grants

Grants are another form of free money that is provided by the federal government, state governments, and individual universities. Grants are entirely need-based and can be used to cover a various educational costs. The US Department of Education is the largest provider of grant aid and operates four different grant programs. Some examples of scholarships and grants are discussed below.

Work-Study Programs

Work-study is a program that allows students to earn income to offset college expenses through part-time employment with their university. The Federal Work Study (FWS) program is the largest in the country and is available at approximately 3,400 postsecondary institutions. The program is open to undergraduate, graduate, and professional degree students who demonstrate financial need and are enrolled either part- or full-time. Employment opportunities vary by university, but FSW positions are traditionally related to the student's major concentration or in service and civic-oriented occupations. The total amount of work-study aid depends on the student's financial need and the amount of funding available at each institution. The estimated award amount for FY14 and FY15 is $1,678, according to the Catalog of Federal Domestic Assistance.

Employer Tuition Reimbursement

Through employer tuition reimbursement programs, employers help pay for their employees' college education including tuition, fees, books, supplies, and equipment. The maximum annual tax-free benefit is $5,250. According to the IRS, employer educational assistance does not cover transportation, meals, lodging, tools, or supplies that students keep after completing the instructional course. If employers provide more than $5,250 in annual educational benefits, any amount over the maximum is subject to income tax. To be eligible to receive employer tuition reimbursement tax benefits, the plan must be in writing and meet other government requirements. More detailed information on employer tuition reimbursement, as well as other tax benefits for education, can be found in IRS Publication 970.

Tax Credits and Deductions

The IRS also provides a number of programs designed to decrease the tax burden on taxpayers' higher education expenses. The two most common types of tax savings for college costs are credits and deductions.

Credits

There are currently two education credits available:American Opportunity Tax Credit (AOTC).

A credit for qualifying educational expenses paid for an eligible student during the first four years of college. The maximum annual credit is $2,500, for a total of $10,000 over four years. If the credit brings the payer's tax amount to zero, he or she may have 40% of the remaining credit refunded (up to $1,000).Lifetime Learning Credit (LLC).

LLC is a credit that can help pay for undergraduate, graduate, and professional degree courses. It is worth up to $2,000 per tax return and there is no limit on the number of years that this credit can be claimed.

Eligibility:

- Taxpayer, their dependent, or a third party pay for qualified higher education expenses

- The student be enrolled at an eligible education institution

- The credit holder is the student or the spouse or dependent of the student

Deductions

Education-related tax deductions can take several forms. The two most common are:Tuition and fees deduction.

The tuition and fees deduction can reduce an individual's taxable income by up to $4,000. The taxpayer may choose to take this deduction or one of the above-discussed credits depending on which one provides the biggest tax break. Student loan interest deduction.

Generally, personal loan interest (other than mortgage interest) is not deductible. However, if a person's modified adjusted gross income is less than $75,000 (or $150,000, if filing jointly), a special deduction is allowed for paying interest on a student loan. This deduction can reduce the amount of income subject to tax by up to $2,500.

Ways to Reduce College Costs

The best way to avoid huge student loan debt is to start saving early in order to avoid having to rely on student loans. Students and parents who create a financial plan early on and start saving through education-related savings programs will find themselves saving a fortune in college costs. Below are some steps students and families should consider throughout the college journey.1

Before and During High School

Start saving by taking advantage of 529 Plans early on.

529 Plans are tax-advantaged savings plans that encourage future college students, their parents, and just about anyone else to start saving for college early. Every state and the District of Columbia has at least one 529 plan available to its residents. Plan details and eligibility requirements vary widely, but there are two basic types:

Prepaid tuition plans allow savers to purchase college units or credits at participating colleges and universities at current rates and use them in the future.

College savings plans allow savers to establish accounts for designated beneficiaries to pay for their college expenses. Take Advanced Placement classes while in high school.

Advanced Placement (AP) classes allow high school students to complete college-level courses and earn college-level credit. Earning AP credit reduces the number of credits students must complete in college, which in turn can shorten the amount of time to graduation and reduce the total cost of earning a degree. Take online college courses to get a head start.

A huge number of four-year institutions (and some two-year colleges) offer degrees online allowing students to avoid the costs of moving to away from home and paying for a dorm room or apartment. High school students can also take online college courses to get a head start and reduce their time to graduation. Find a job.

Many high schoolers find part-time and summer jobs in their hometowns, mostly to pay for personal expenses, extracurricular activities, and fun. Instead, prospective college students can use that income to help defray the cost of college.2

When Choosing a College or University

Choose an in-state college.

The lure of the open road can be pretty enticing to a student right out of high school, and that's OK. Just remember to stay within the borders of your home state when considering a public college or university as in-state tuition rates are significantly lower than out-of-state rates and state resident students can save a bundle compared to those coming from outside for the same quality-level education. Some states even offer tuition-free college for students who attended high school in-state and go on to attend a local college or university. Take advantage of state and/or regional tuition discounts.

Not all colleges and universities charge out-of-state students higher tuition rates. There is a growing trend of schools offering tuition discounts to students coming in from across state borders. Consider fixed-tuition degree programs.

One of the biggest problems with a questionable economy is predictability. It's hard to tell how time will impact the costs of college. With that in mind, a significant number of schools are offering fixed tuition programs as a way for students and their parents to lock-in current tuition rates and avoid increases in the future. Live at home to avoid campus-housing costs.

For students and families on a tight budget, the savings from living at home and not paying room and board expenses at a university can add up quickly, in a good way.3

While in College

Enroll in accelerated programs.

Reducing the time it takes to graduate can save money. Most colleges and universities today offer accelerated degree programs and courses that allow students to do just that. Accelerated courses are shorter in time length but not in material covered, so students will need to be diligent in their studies and not fall behind. Take summer school classes.

Summer school classes allow students to earn a greater number of credits quickly, reducing the time it takes to graduate. Tuition during the summer is often less expensive than the traditional school year and is another way for students to save money. Work as a tutor.

For high achieving students, working as a tutor allows them to earn income while helping their peers. Get used or shared textbooks or rent books.

One of the bigger "sticker shock" items for college students is the cost of textbooks and other class materials. Students can fight back by purchasing used textbooks, sharing textbooks with classmates, or renting them through programs offered by groups such as Chegg. Create a budget and think outside the box to cut back on spending.

Practice thrift. Smart spending saves money. Stay home and cook. Cut coupons. Don't use credit cards. Skip the gym membership and workout outdoors on your own. Attend free events on campus for entertainment. Take advantage of student discounts. Get together with your friends and buy groceries in bulk. Change your cell phone plan. You get the idea. There are number of ways that college students can cut costs. Even a small discount can help and over time, it all adds up.4

After Graduation

If you have loans, pay more than the minimum amount due each month.

When your monthly student loan payment comes around, try to pay more than just the minimum amount. Every time you do, you are reducing the principal amount of the loan resulting in lower total interest paid. Borrowers who do this consistently can save thousands of dollars over the course of the loan. Don't miss any loan payments.

Getting behind on loan payments can cause serious problems, particularly to credit ratings. A bad credit rating means that you may have to pay more for things you purchase in the future such as a car or house. Develop a budget and stick to it.

This can be a tough one for a graduate just beginning to collect a professional paycheck and wanting to cash in on all of those hard years of sacrifice in college. Dig deep, discipline yourself and put off the instant gratification for a few more years. The result will be more total gratification in the long run. Consolidate any debt.

If you have more than one student loan to pay off or if you have a student loan and other sources of debt such as credit cards or car payments, see if you can consolidate your debts into one smaller monthly payment. Consolidation may mean a lower monthly payment with a longer payoff time, but a longer payoff time is better than missing payments or facing a default. Explore public service careers.

Students with loans through the William D. Ford Direct Loan Program may be eligible to participate in the Public Student Loan Forgiveness (PSLF) program. The PSLF is a federal government program created to help professionals have their student loan debt forgiven in return for a period of full-time public service work. In order to have one's loans forgiven, the borrower must make 120 on-time, full monthly payments under a qualifying repayment plan. Only jobs in specified Federal, state, and local public offices and some non-profit organizations designated by the IRS are eligible.

Student Loan Debt Facts

In the last decade and across the nation, student loan debt has become a concern among prospective and current students and especially recent graduates. Here are a few facts and statistics that illustrate just how serious student debt in the United States has become:

The Reality of Higher Tuition Costs

"If over the past three decades car prices had gone up as fast as [college] tuition, the average new car would cost more than $80,000." Source: The Real Reason College Tuition Costs So Much (NYTimes.com, April 4, 2015)

The Reality of Student Loan Debt:

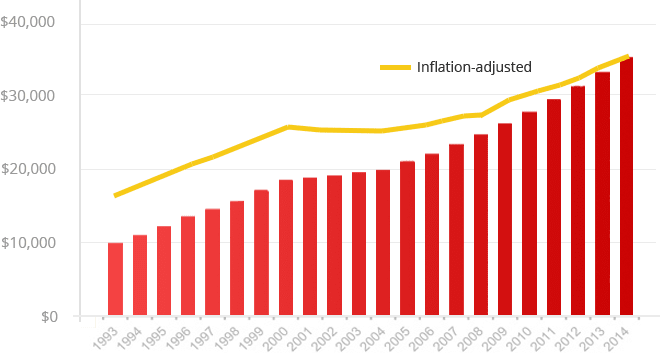

The average debt load for a 2014 college graduate with student loan debt is $33,000, nearly twice as much as it was 20 years ago, even adjusting for inflation. Class of 2014

Average debt per borrower in each year's graduating class.

Source: Congratulations to Class of 2014, Most Indebted Ever (Wall Street Journal, May 16, 2014)

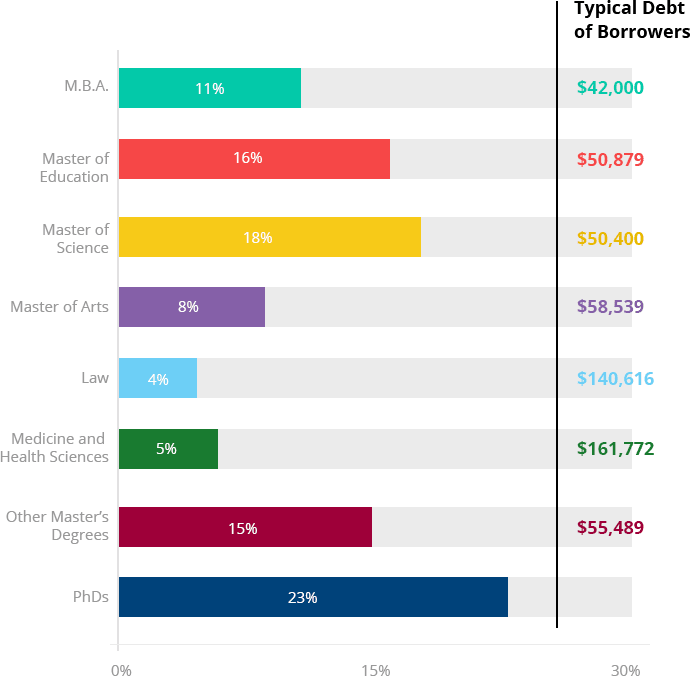

Since 1999, the amount of student debt in the US has increased by 500 percent Source: The Huffington Post Combined undergraduate and graduate debt

(2012 completers) Debt of All Graduate Borrowers at the 50th Percentile

Debt of All Graduate Borrowers at the 50th Percentile

Includes all graduate programs including PhDs. All figures in 2012 dollars.

Source:New America, The Graduate Student Debt Review, March 2014

Resources

Financial Aid & College Affordability

CareerOneStop is a an online resource offered by the U.S. Department of Labor and has a scholarship, grant, fellowship, and internship database that is searchable by keyword, award type, location, level of study, and individual affiliations.

College Affordability and Transparency Center

Here, students, parents, and policymakers can find information on college costs. There are also several lists of institutions based on tuition and net prices. All lists are in accordance with the Higher Education Opportunity Act and are updated every year.

Free Application for Federal Student Aid

The online portal for the FAFSA®, this resource includes a college search option, advice for filing out the FAFSA®, and customer service representatives that can help walk parents and students through the process.

Parents and students can get information about student loans, grants and federal work study through the US Department of Education.

TEACH grants can help prospective students pay for college if they plan to become a teacher.

Save on Textbooks

Amazon allows users to buy and sell textbooks, as well as rent. eTextbooks are also available for purchase or rent. Students can take advantage of free two-day shipping by signing up for Amazon Prime (at 50% off the regular fee, after a free six-month free trial).

This site helps students find the lowest prices for new and used textbooks. Students can buy textbooks and save up to 90%, rent and return when done, or sell textbooks for cash.

Chegg offers an online marketplace for students to rent, purchase, and sell textbooks.

Half.com, an eBay company, is another source for buying or renting college textbooks at a lower cost. Students can search by title, author, keyword, or ISBN and can also sell textbooks that they no longer need.

Military and Veterans

The Office of Federal Student Aid provides basic information on scholarships, grants, and other financial aid for military personal, Veterans, and their families.

Users can join military.com for free to gain access to news and information on government benefits, scholarships, where and how to find a mentor, and much more.

Funded by the Department of Defense, this comprehensive site offers information on all aspects of military life, such as deployment, employment, education, parenting, and more. Users can access free resources, products, articles, and tips, as well as call a confidential 24-hour line for services.

National Military Family Association

NMFA strives to represent service members and their families on Capital Hall, at the Pentagon, and Veterans Administration. Service members and their family members can find information and resources on various topics, including scholarships, education, careers, and much more.

This site provides information, news, and resources for veterans, service members, and communities. Visitors can find detailed information on the GI Bill, state benefits, and more.

The DOE offers information and resources on higher education specifically for military families and Veterans. Get more details on the Yellow Ribbon Program, Post 9/11 GI Bill, and other education benefits, programs, and services.

U.S. Department of Veterans Affairs

Current, retired, and dependents of military service members can learn about the various educational and training benefits, and more, offered through the U.S. Department of Veterans Affairs.

Related articles that may interest you

Best Master's in Data Analytics Programs: What You Need to Know

Top Online MBAs in Business Analytics

Explore the top online MBAs in business analytics, including tuition costs, curricular offerings, and more with this student research resource.

Scholarships and Financial Aid in Texas

Financial aid makes college a reality for many students. Learn about the top scholarships in Texas and how you can earn one.

AffordableCollegesOnline.org is an advertising-supported site. Featured or trusted partner programs and all school search, finder, or match results are for schools that compensate us. This compensation does not influence our school rankings, resource guides, or other editorially-independent information published on this site.

Do this for you

Explore your possibilities- find schools with programs you’re interested in and clear a path for your future.